The Eaton Fire Claim Deadline* Is Approaching. Get Help Now.

You know the old maxim: Hope for the best, plan for the worst. Although we don’t expect a catastrophic event like a fire to destroy our homes, we take out homeowners or renter’s insurance. While we hope for long life, the threat of an unforeseen injury or illness is why we pay for health insurance. For the same reasons, state laws require drivers to obtain car insurance.

But the fact that the law requires it does not mean that every driver has a sufficient policy. In some cases, drivers have no policy at all. If you do have an auto accident with an uninsured driver, that does not necessarily mean that you can’t recover for your damages.

However, to create the best possibility for recovery against an uninsured driver, you can plan for the worst by obtaining your own uninsured or underinsured motorist insurance policy.

Uninsured and Underinsured Motorist Policies

Not every driver has sufficient car insurance. One survey found that as many as 13% of drivers, or one in eight, do not have any insurance at all. This leads those who do to wonder, “Will my insurance cover an uninsured driver?”

In either case, you can take out your own supplemental insurance to cover any shortfall.

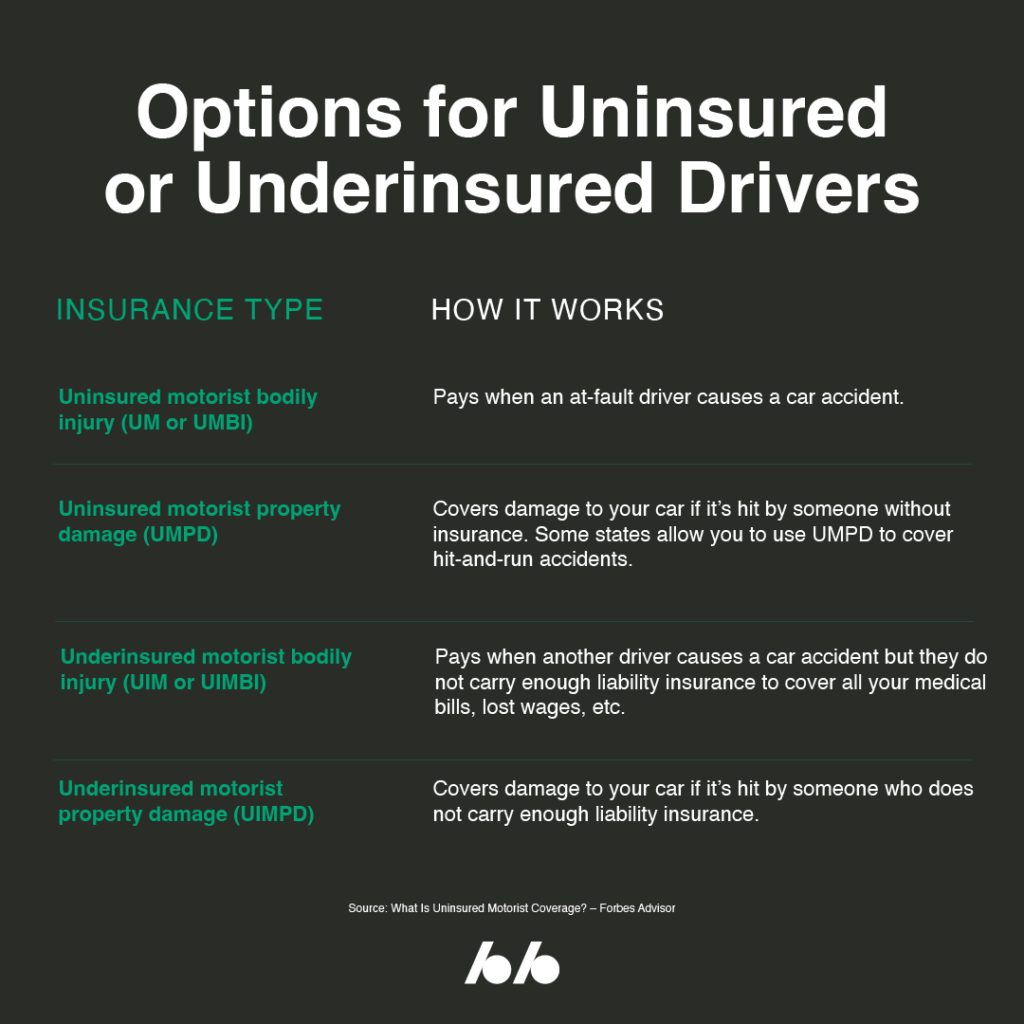

Uninsured Motorist Insurance

An uninsured motorist insurance (UM) policy is intended to prevent you from spending your own money for injuries or property damage in an auto accident that you did not cause. This type of policy will pay your car repair and medical costs when the other driver is at fault but does not have liability insurance of their own.

Uninsured motorist insurance covers damages when the other driver is at fault and has no insurance.

Moreover, a UM policy will cover:

- Injuries or damages suffered by you, family members in your household, or passengers suffer

- Medical bills, pain, and suffering, lost wages due to missing work, and funeral expenses (if bodily injury policy)

- Damages to your car or personal property, but you may have a deductible (if property damage policy)

The coverage offered by a UM policy varies by state and insurance carrier. For example, you may purchase a bodily injury UM policy and/or a property damage UM policy. These options provide you with wider recovery options.

In any case, UM coverage is expressed as two numbers. Take 100/300, for example. Such a policy would mean that anyone involved in the wreck would be covered for up to $100,000 in bodily injury claims, but that policy would max out at $300,000 per accident.

So if you had four people in your car during an auto accident with an uninsured driver, a $300,000 limit might not be enough. In some cases, your health insurance policy may make up the difference.

Underinsured Motorist Coverage

Unlike uninsured motorist policies, underinsured motorist coverage (UIM) pays for the difference between another driver’s insurance coverage and the extent of your damages when their policy is insufficient. But just like UM policies, a UIM policy only kicks in when the other driver is at fault.

Is UM or UIM Coverage Mandatory?

Whether UM or UIM coverage is mandatory depends on your state’s laws. While a few do require such coverage for every driver, most do not. But even those states that do not require UM/UIM coverage do require that insurance providers offer such coverage.

For example, California does not require its drivers to purchase UM or UIM insurance. However, insurance companies operating in the state must offer such coverage for sale.

Whether you should purchase either UM or UIM coverage, however, is a different question. Consider whether your state has a higher than average number of uninsured drivers. In California, for example, almost one in five drivers are uninsured. But in Mississippi, about 30% of drivers have no insurance.

Other factors to consider include:

- Whether you have adequate health insurance or a high deductible

- Whether you expect to be recompensed for pain, suffering, and lost wages, which health insurance doesn’t cover

- Whether you have sufficient collision insurance coverage

If you do decide to purchase UM or UIM insurance, a key rule of thumb is to purchase coverage in at least the same amount as your liability limits.

Other Types of Car Insurance

In addition to UM and UIM policies, other supplemental car insurance policies can make up the difference between your damages and an at-fault driver’s lack of insurance.

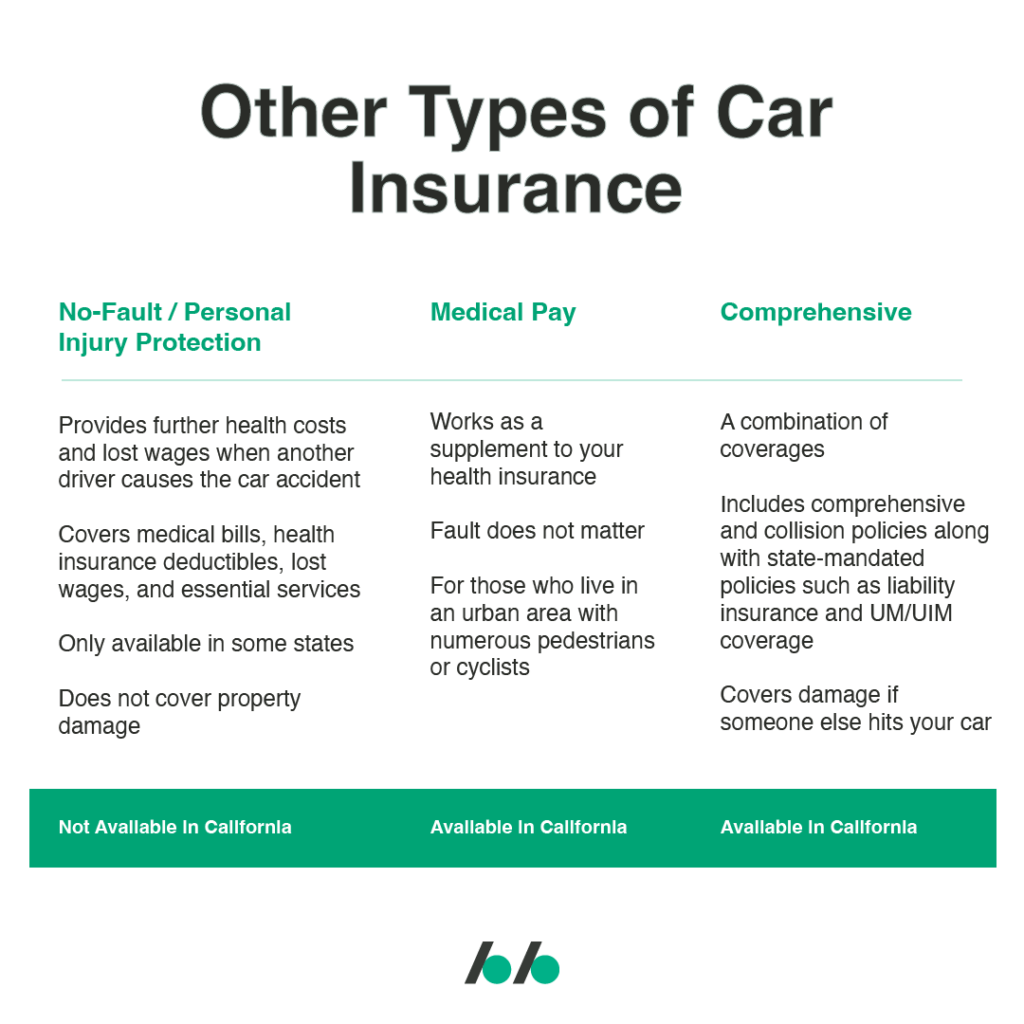

No-Fault or Personal Injury Protection Policies

Like UM/UIM coverage, personal injury protection (PIP) policies, also known as no-fault policies, provide further health costs and lost wages when another driver causes a car accident. PIP policies cover medical bills, health insurance deductibles, lost wages, and essential services (e.g., child care, cleaning, grocery shopping, etc.).

However, PIP policies are only available in a handful of states and do not cover property damage.

Medical Pay Coverage

Different from a PIP policy, medical pay (MedPay) insurance works as a supplement to your health insurance. Fault does not matter, and this policy will kick in even if you were driving under the influence of drugs or alcohol.

You may consider adding MedPay if you live in an urban area with numerous pedestrians or cyclists as well.

Comprehensive Coverage

Complete car insurance coverage refers to a combination of coverages including comprehensive and collision policies along with state-mandated policies such as liability insurance and UM/UIM coverage.

Electing for collision coverage as well will cover damage if someone else hits your car.

Car Insurance and Hit-and-Run Accidents

Liability and UM/UIM insurance policies cover typical car accidents and those where the other driver lacks sufficient insurance. However, what happens when you’re involved in a hit-and-run?

A hit-and-run accident occurs when the other driver leaves the scene without exchanging insurance or contact information. Whether insurance will cover the damage depends on the type of insurance available in your state.

If your state allows uninsured motorist coverage for property damage claims, then the insurance carrier may cover hit-and-run accidents.

But even where UM property damage coverage is allowed, you may have to pay a deductible. Nonetheless, collision coverage may cover your car damage.

How to Collect Money from an Uninsured Driver

Uninsured or underinsured driver insurance is used to cover the gap between what the at-fault driver can pay and the extent of your damages. But the reality is that most people who lack car insurance do so because they can’t afford it. Suing an uninsured driver for your damages, therefore, will not likely sufficiently compensate you.

Seeking recovery from your UM or UIM policy is a more fruitful route. In a case relying on UIM coverage, you’ll receive an amount bridging the gap between the underinsured driver’s policy and your damages. Generally, you will not get the full amount of your UIM policy plus the driver’s liability coverage.

But you should view the UM/UIM provider as an adversary in the insurance claims process. The provider will likely fight your claim – expect them to investigate your medical treatment, injuries, and other information.

Adamson Ahdoot Can Help You Recover Against an Uninsured Motorist

When you’ve done your part to plan for the worst by maintaining sufficient car insurance, an auto accident with an uninsured motorist can seem unfair and leave you wanting adequate compensation for your bodily injuries and property damages. But that’s what uninsured or underinsured motorist coverage is for.

Even then, fighting your UM/UIM carrier and the other driver to cover your damages can be difficult without a trusted partner. At Adamson Ahdoot Injury Attorneys, our team has the experience necessary to fight for you.

Adamson Ahdoot’s attorneys have fought for people involved in auto accidents with uninsured drivers. Get a free consultation or have your questions answered today.

Blog

California Fireworks Injuries After the Fourth of July 2026: Recent Accidents and Liability

The Fourth of July is one of the biggest holidays for fireworks in the United States, but...

$176M Verdict, LAUSD Sexual Abuse Allegations, and Major Negligence Claims

California’s June News Highlights Institutional Liability Cases, Serious Traffic Acciden...

What Damages Can Be Included in an Eaton Fire Claim?

One of the biggest misconceptions after a wildfire like the Eaton Fire is that a homeowner...

New Evidence in the Eaton Fire Investigation: What It Could Mean for Wildfire Lawsuits Against Edison

New Surveillance Footage Could Provide Key Information About the Cause of the Fire and Cha...

How the Southern California Edison Claims Process Works: Step-by-Step Guide for Eaton Fire Victims

Following the Eaton Fire, many residents in Altadena, Pasadena, and other affected communi...

Google’s $50M Settlement, $450K Dog Bite Case, and $7.5M Truck Crash Lawsuit

California's May News Highlights E-Bike Liability, Hospital Sexual Abuse Lawsuits, and Wil...

Should Eaton Fire Victims Accept Edison Settlement Offers?

Following the Eaton Fire in January 2025, Southern California Edison (SCE), the utility co...

Uninsured Drivers and Motorcycle Accidents in California

In California, victims of motorcycle accidents caused by uninsured drivers may suffer seri...

Fatal Motorcycle Accidents: Wrongful Death Claims in California

A motocross rider speeding across a dirt track, kicking up dust mid-jump, capturing high-i...

Motorcycle Accident Injuries: Long-Term Medical Costs and Compensation

A parked motorcycle along a quiet road at sunset, with warm light casting long shadows, ev...

Table of Contents

Other Practice Areas

Accidents

- 5 Common Types of Car Accidents

- Accident Reconstruction in Los Angeles

- Amazon Product Defect Injury

- Assault Injury Lawyer

- Attorney Regarding Uber Accident

- Aviation Accident Lawyer

- Bakersfield Bus Accident Lawyer

- Bakersfield Car Accident Lawyer

- Bakersfield Motorcycle Accident Lawyer

- Bakersfield Rideshare Accident Lawyer

- Bakersfield Truck Accident Lawyer

- Boat Accident Lawyer

- California Institution for Women Sexual Abuse (CIW) Lawsuits

- California Metro & Railroad Accidents

- California Women’s Prisons and Jails Sexual Abuse Lawsuits

- Can an Uber Driver Sue Uber

- Car Accident Lawyer

- Car Accidents at Night

- Carnival Ride Accident Attorney

- Century Regional Detention Facility (CRDF) Sexual Abuse Lawsuits

Injuries

- About Brain Injury Lawsuits

- After Head Injury

- Amputation & Disfigurement Injury Lawyer

- Back Injuries from Car Accidents

- Brain And Spinal Cord Injuries Lawyer

- California Dog Bite Injuries

- California Dog Bite Laws

- California Wrongful Death Attorney

- Chronic Pain

- Common Back & Neck Injuries

- Common Types of TBI

- Dangerous Dog Breeds

- Delayed Pain

- Dismemberment or Amputation Injury

- Dog Bite Attorney in California

- Dog Bite Damages

- Dog Bite Injury Lawyer

- Dog Bite Liability

- Dog Sitter Dog Bites

- Football Head Injuries Lawyer

Related Case Results

Get a Free Consultation:

(424) 392-7649

Connect with an Attorney

Fill Out the Form Below

"*" indicates required fields

By submitting this form, you agree to be contacted and recorded by Adamson Ahdoot LLP or a representative, affiliates, etc., calling or sending correspondence to your physical or electronic address, on our behalf, for any purpose arising out of or related to your case and/or claim. Standard text and/or usage rates may apply. If at any time you wish to opt out of communication, reply “STOP.” Text “HELP” for assistance. Message frequency may vary. See the privacy policy and Terms and Conditions on the webpage.