Signing up for car insurance is overwhelming. You just want to make sure you are protected without overpaying, but what kind of coverage do you need? Understanding the terms that insurance companies use and the types of coverage that they offer can help you make decisions about how to best protect yourself.

At first glance, it may seem strange that your policy has both bodily injury and personal injury coverage. The two terms sound like they are describing the same thing, but they actually do cover two different circumstances and protect you in different ways.

Comparing Bodily Injury vs. Personal Injury Insurance

Although bodily injury and personal injury insurance are similar, there are some differences. They both compensate for medical expenses from an injury after a car accident, but they cover different people and pay out under different rules. Both types of coverage protect you, just in different ways.

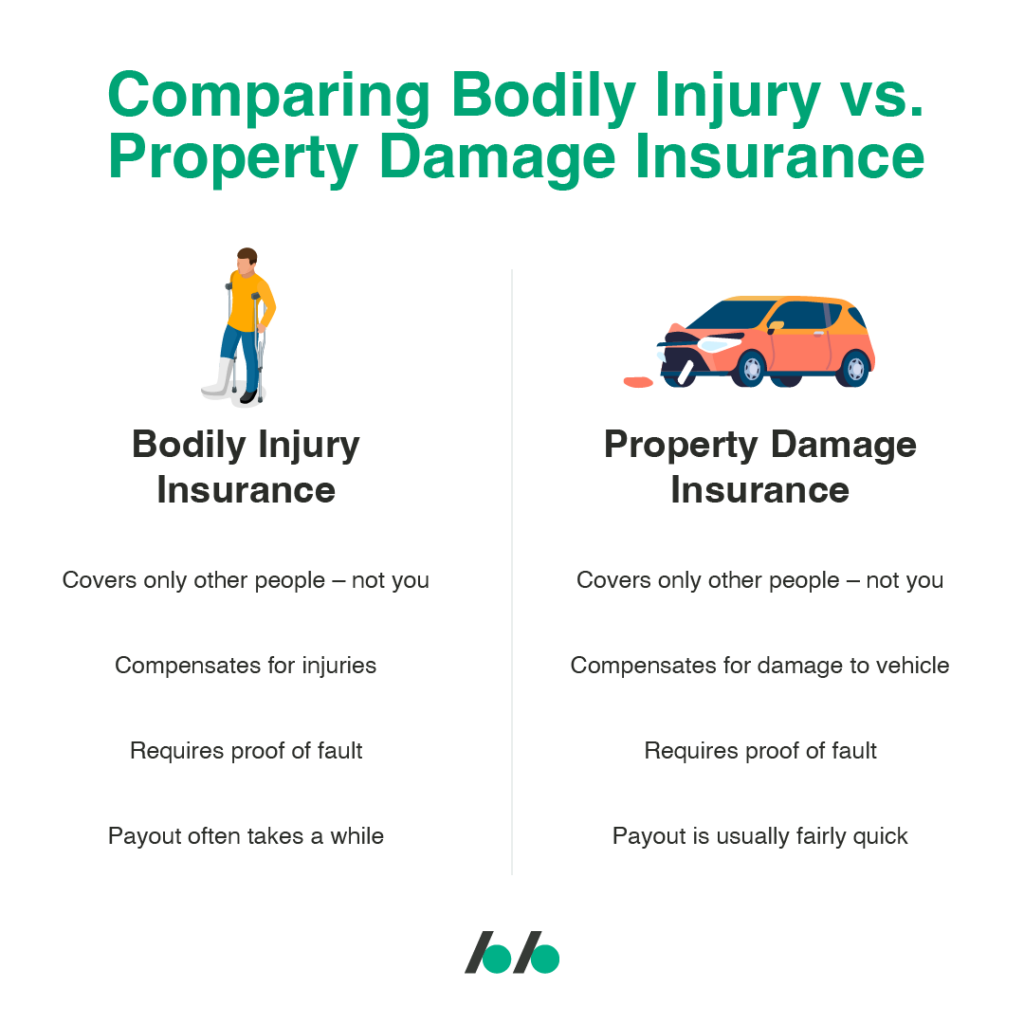

Bodily injury coverage, also called liability insurance, pays for other people’s medical costs resulting from a car accident that you were at fault for causing. The coverage includes passengers in your car, pedestrians, and people in other vehicles. All kinds of injuries are covered by bodily injury insurance.

Bodily injury insurance compensates anyone other than you for injuries they receive in a car accident that you caused.

It’s important to note that liability insurance actually has two parts: bodily injury and property damage coverage. We will discuss property damage coverage a bit more down below.

Bodily injuries include anything from simple cuts and bruises to broken bones, to seriously disabling or life-threatening injuries. If you or someone else requires medical treatment after a car accident, then that is a bodily injury, even if it is relatively minor.

A bodily injury liability policy will compensate the injured party for medical bills, lost wages, and disabilities from these types of injuries. The coverage can also include loss of income, pain and suffering, reduction in quality of life, and funeral costs.

Liability insurance is required in California, but even if it wasn’t, it would be important to have it. Beyond covering the injuries of your passengers and anyone else involved in the accident, it protects you. If you cause an accident, you can be personally liable to the injured parties, and they can sue you to pay for their injuries. Bodily injury coverage is your best line of defense against that. Under this policy, your insurance will defend any suit against you, covering your lawyers’ fees, and will pay any judgment against you up to your policy limit.

Liability insurance covers other peoples’ injuries, but it also protects you by covering claims and lawsuits against you.

Even in circumstances where you are not at fault or are only partially at fault, this coverage is invaluable. If you are not at fault, your insurance will still defend you, working to prove that the accident was caused by someone or something else. And in the circumstance where multiple people share the blame, your insurance will cover your portion up to policy limits.

California requires that you carry a minimum amount of liability coverage but choosing to raise that policy amount can help protect you. With even minor or moderate injuries, the cost of medical treatment can quickly exceed the policy limits. In the case of a severe injury, minimum limits likely won’t come close to covering the medical expenses. In those cases, the injured party can come after you personally for the amount that their bills are not covered by the insurance policy. A higher policy limit can help ensure that never happens to you.

Personal Injury Protection (PIP) is no-fault insurance that covers you and your passengers’ medical bills if you are injured in a car accident. This type of policy is referred to as “no-fault” because it doesn’t matter who or what caused the accident, you are always covered. A PIP policy compensates you for all the same kinds of injuries as bodily injury liability coverage. The difference is who is covered and how easily the policy pays out.

PIP insurance covers your medical bills, regardless of who caused the accident.

The no-fault aspect of PIP means that it pays out faster and easier than bodily injury coverage. If you are in a car accident that someone else caused, receiving compensation from their bodily insurance policy can take a considerable amount of time. The parties and insurance companies have to come to an agreement about where the fault lies, or if they can’t then the case may have to go to court. On top of that, they will only pay out in one total payment, so the full extent of the injuries must be understood and proven before you will receive any compensation. An attorney can help you with your car accident injury claim, but the process will still take time.

With a PIP policy, claims processing won’t be necessary. Simply showing proof of your medical bills to your insurance will get you reimbursed quickly and easily. You can often submit individual bills for reimbursement until your policy maximum is reached.

PIP will reimburse you for doctor and hospital visits, ambulance fees, and prescriptions. Depending on your individual policy, it may also cover other expenses such as a percentage of lost wages, hiring services because of your injuries (such as a home cleaning service), or funeral expenses.

Your PIP policy can be used in conjunction with your health insurance policy to cover your deductible, co-pay, or other medical expenses not covered by your health insurance.

PIP policies typically have a per-person maximum between $2,500 and $10,000, with $10,000 being the upper policy limit allowed by most insurance companies.

This coverage is not required in California, but it can be a very useful add-on to your car insurance policy. It is typically inexpensive and often well worth the cost. Making sure your PIP’s per person maximum is more than your health insurance deductible can help ensure that you get the treatment you need after a car accident.

How is Property Damage Insurance Different from Bodily Injury Insurance?

Like bodily injury coverage, property damage insurance is a part of your liability insurance policy. You are required to carry it under California law, and it covers other people but not you. So, how is it different from bodily injury coverage?

Property damage coverage pays for the damage to other peoples’ cars and other personal property after an accident that you caused. The vehicle is likely to be the largest part of this kind of claim, but the policy does cover other property damaged in the accident, including eyeglasses, laptops, or work equipment.

If you are at fault in an accident, the property damage part of a liability policy covers repair or replacement of other peoples’ cars and damage to other personal property.

In California, the minimum property damage coverage you are required to carry is quite low. Like bodily injury coverage, choosing to raise that minimum can help protect you by ensuring that your policy fully covers the other driver’s claim. Otherwise, they can come after you personally to make up the difference.

It’s also important to note that liability insurance does not cover any damage to your own vehicle or personal property. For that kind of coverage, you are going to need a collision policy.

Property damage and bodily injury claims are handled completely separately for the same accident. Property damage claims typically pay out much more quickly and easily. It’s just simpler and faster to get a clear picture of the total value of a property claim (the cost to repair or replace the vehicle) than it is to determine the full extent and cost of a personal injury claim.

Protect Yourself with a Solid Car Insurance Policy

Understanding the types of insurance available to you and making smart choices when setting up your auto policy can help protect you and your loved ones if an accident happens. Whether you are at fault or not, the important thing is that your policy is working to protect you. If you’re unsure about whether your insurance covered you in an accident, one of the knowledgeable attorneys at Adamson Ahdoot can walk you through your options.

If you or someone you love has been injured in a car accident due to the negligence of others, the accident attorneys at Adamson Ahdoot LLP may be able to help. Call (800) 310-1606!